This article first appeared in AdNews in-print. Click here to subscribe to the AdNews magazine or read the iPad edition here.

We're looking at a busy year with media de-regulation potentially kicking off a M&A spree plus revenue boosts from the Olympics and elections. On a less favourable note, the industry will have to contend with a fragmenting business, the ongoing problem of adblocking and viewability all against a backdrop of continued chatter around agency transparency. Looking for a dull moment? You won't find one in this year. Here's 10 things that are on the agenda in 2016. Nicola Riches reports.

1. Media Regulation

Australia has been waiting for a long time for the current media laws to be reviewed and finally, in the second week of January communications minister Mitch Fifield, signalled that government is expected to present new draft laws in quarter one.

It is widely thought that the 'Reach Rule' or the 'Two out of Three Rule' limiting the number of media outlets one organisation can own will be scrapped, but most likely with a caveat that local news and current affairs production will be protected and some form of quota will be introduced. Fifield has gone on record saying he has already engaged the Coalition, opposition and all commercial entities before drafting new laws, meaning that it should all pass smoothly. Depending on the 'local caveat', it should trigger a very interesting wave of mergers and acquisitions, many of which have already been the subject of speculation.

2. Transparency

The issue of transparency is not going anywhere. In response to the debacle that surrounded the issue last year, the Media Federation of Australia - in association with PwC - set out its first instalment of industry guidelines towards the close of 2015.

Widely acknowledged to be little more than a document detailing mere terms of reference, it provided members with some explanation of the terms that arise when the issue of transparency rears its head, such as media agency transparency rebates, agency, commissions, value banks, ethics training and agency trading desks. The MFA will follow it up with another guideline document at some point in the near future, but until then the onus lies with agencies to review, or simply strengthen, practices.

3. Digital/Viewability/AdBlocking

The position of digital as the second largest ad segment by billings in the Australian market is now cemented and mobile and video advertising should continue to grow at healthy rates as they move mainstream. Agency bookings for digital, according to SMI, grew 19.1% last year.

With regards to viewability and trackable viewable impressions, it is still a time of transition in Australia: technology and practical elements such as billing systems have to catch up. IAB CEO Alice Manners says it will be one of 2016's biggest hurdles. GroupM has skirted the IAB with its own deals with nine publishers to promise to deliver 100% viewability and IPG Mediabrands has also made moves towards it.

Meanwhile, adblocking will present a doubleedged sword. There will be, say many in the industry, an increased pressure to educate consumers as to the role of the ad-funded, online economy, but also an increased need for publishers to heighten and optimise the user experience so that ads become synonymous with quality content.

4. Social

Chief concern for all social networks this year will be audience retention. Twitter is widely-known to be suffering user migration, so too Facebook which has reportedly seen a drop off of younger users. On the plus side however Instagram, Pinterest and Tumblr are still keeping pace. Facebook, Twitter, Instagram, Pinterest and LinkedIn all made serious investments into their advertising platforms in 2015, with new features offering more ways for brands connect with audiences and that investment will show rewards this year.

It’s widely believed social platforms are a heartbeat away from becoming retail environments where consumers can purchase without leaving the networks: Facebook’s shops, Twitter’s ‘buy’ button and Pinterest’s Buyable Pins are all examples, while Instagram introduced clickable links and is moving ever closer to e-commerce.

Elsewhere, video will continue to be central to all social media strategies, with much talk at CES this January about the development of vertical video. Mobile video consumption is indeed still on the rise – 35% of respondents in July 2015 to an IAB survey reported watching more video on their smartphone than the year previous, and that is likely to grow again this year.

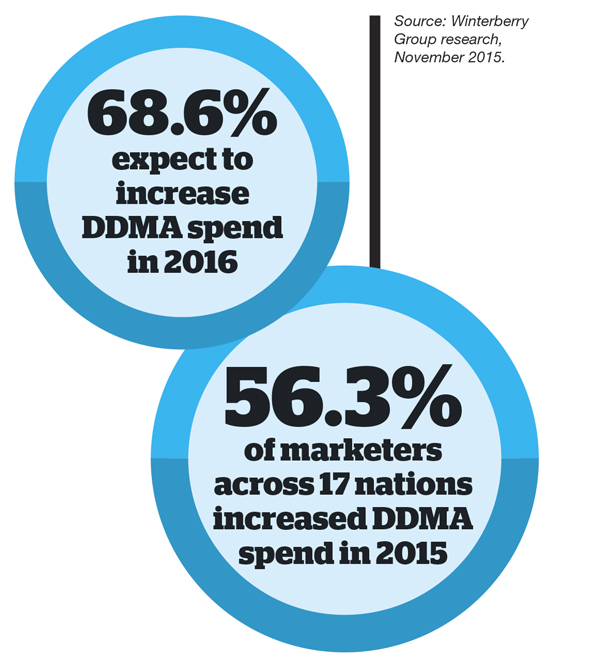

5. Data-Driven Marketing and Advertising

A study conducted by the Global Alliance of Data-Driven Marketing Associations (GDMA - an alliance of 27 independent marketing associations around the world, including the ADMA locally) and US research and consulting firm Winterberry Group indicates that 74.1% of marketers remain confident in the value of datadriven marketing and advertising (DDMA) and its potential for future growth. However, what’s interesting to note is that figures are slightly down on 2014 levels (63.2% increased their respective spending on the prior year).

The year-on-year dip could reflect the finding that participants cited improved measurement and attribution techniques have already allowed them to streamline DDMA processes. Meanwhile, 2016, it is thought, could be the year that more and more major brands take data in-house and cut back on the number of agencies on retainer.

6. Radio

Radio showed steady gains in 2015 and that looks set to continue during 2016. Last December's SMI data showed a year-on-year increase of 7.8%. It is believed radio will maintain similar growth next year. It is also thought that 2016 will see talent finally settling down after a couple of years of musical chairs across the board that kicked off with Kyle and Jackie O's move from SCA to ARN in 2013.

Commerical Radio Australia CEO Joan Warner puts the switches down to a “cyclical event”, but predicts that DJs will more than likely keep their current posts. This means Sam Frost and Rove McManus will continue to try and prove their worth at 2DayFM, while returning pair Hamish and Andy – while holding poll position in Melbourne – will continue to strike for a better placing in drivetime for Sydney.

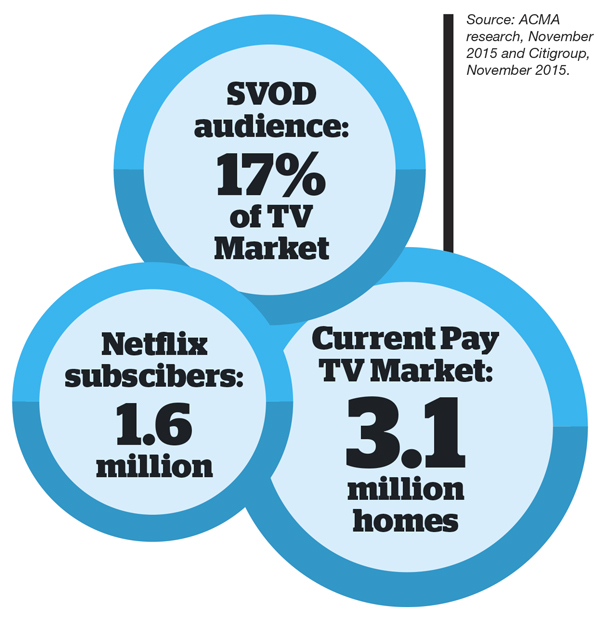

7. TV - FTA and subscription

Ten/Foxtel/MCN will bed-in and market expansion could define the next 12 months.

Citigroup believes that the next two years will be crucial: that Foxtel will reach 35% market penetration and remain the premium provider of sports and drama. Last year was the year that SVOD invaded as Stan and Netflix launched. This year will be the year that it shakes out. Citigroup’s expectation is that SVOD will poach a 10% share of the free-to-air market. “Not great but not a train wreck,” says former Citi analyst Justin Diddams. Seven chief revenue officer Kurt Burnette said 2015 will go on record as the largest ever year for advertising revenue for FTA, but that could be surpassed in 2016 owing to the Olympics and elections.

Broadcasters are of course diversifying into digital through streaming and catch-up and more tie ups with social platforms is likely. Meanwhile the highly-anticipated and delayed OzTam Video Player Measurement (VPM) Report is due to be published as we go to print, meaning the first weekly ratings data for catch-up content will be released on 14 February.

8. Outdoor

Outdoor grew by 3.4% in the Australian metro areas last year, and with this year’s Olympics and elections, there’s no doubt that we could witness a substantial spike in 2016. Grant Guesdon, general manager of Move, believes that the next 12 months will see advertisers reap the benefits of closer consumer engagement with the medium, as well as a hefty milliongrowth in the number of digital sites popping up across Australia.

Advertisers and agencies, meanwhile, will – at some point in 2016 – be able to access fresh audience data thanks to the mooted inclusion of Move data into Emma. Furthermore, real time buying and programmatic displays are just some of the areas of growth likely in the next 12 months. The OMA’s development of the industry-wide Automated Transaction Platform is believed to be one of the starting points of that journey.

9. Publishing

Traditional publishing will continue to have a hard time in 2016 but innovation is abundant. Fairfax Media is currently undergoing a restructure of its consumer and trade marketing departments. Bauer currently has no CEO, no director of sales [updated: Fiorella Di Santo named director of sales] no editor for Women’s Weekly and Cleo has just been given the chop.

News Corp continues with a program of diversification – moving into VIP reader events and banking on property sales websites, while readership for local press hangs in the balance where print is concerned. On ths surface it paints a less than pretty picture. However, SMI data for Jan-Dec 2015 shows that media bookings for newspapers slipped 1.2% and for magazines, 0.7%.

10. State-by-State

Melbourne/Victoria is starting to outperform other metros and States. Agency bookings in the region last year lifted 9.4% reaching $2.6bn. Sydney, meanwhile, was a close second witnessing an upsurge of 2.3% to $3.9bn.

SMI data for Brisbane shows small gains of 1.4%, whereas Adelaide and Perth combined delivered double digit market growth of 12.3% reaching $487.6m, but remain small markets. Carat has this January opened shop in Adelaide, citing the region's strong input from government and of course, the wineries. However, Perth, says 303MullenLowe (which has a strong presence is the city), remains steady but potentially on track for some form of market correction.

Email Nicola at nicolariches@yaffa.com.au.